It was a breakthrough in money transfer history. This transition or more commonly known as, an electronic funds transfer (EFT) would change everything in the payments landscape. ATMs (Automated Teller Machines) were introduced at this point in the course of history.

Money transfer generally refers to one of the following cashless modes of payment or payment systems:

Money order, transfer by postal cheque, money gram or others

It can also refer to the following cash-based wire transfer systems:

al-Barakat, an informal money transfer system originating in the Arab world

Hawala (also known as hundi), an informal system primarily used to send money to and from the Middle East, North Africa, the Horn of Africa, and India, Pakistan, Bangladesh and Nepal

Remittance, a transfer of money by a foreign worker to his or her home country

Electronic funds transfer (EFT) are electronic transfer of money from one bank account to another, either within a single financial institution or across multiple institutions, via computer-based systems, without the direct intervention of bank staff.

According to the United States Electronic Fund Transfer Act of 1978 it is a funds transfer initiated through an electronic terminal, telephone, computer (including on-line banking) or magnetic tape for the purpose of ordering, instructing, or authorizing a financial institution to debit or credit a consumer’s account. [1]

EFT transactions are known by a number of names across countries and different payment systems. For example, in the United States, they may be referred to as “electronic checks” or “e-checks”. In the United Kingdom, the term “bank transfer” and “bank payment” are used, while in several other European countries “giro transfer” is the common term

We are looking for Business Minded people at District level for our startup Project.

A project that has unique feature, advanced business model and huge earning capacity.

Requirement – 1 District Partner from each district of India.

Work Profile – Management & monitoring our platform’s work operations and services in your district.

“Posting content that can be turned into a contest is a great way to gain new followers. For instance, you could post a photo, ask people to caption it and the winner gets a small prize, but to be eligible, you have to follow, like and share. Contests like this expose you to a ton of new users.” –John Turner, SeedProd LLC

2. Content dedicated to special days

“Holidays, both well-known and “weird,” hold universal appeal on the internet and have great potential to attract followers. I have found that posting and celebrating even little holidays, such as “Squirrel Appreciation Day” or “National Cheese Lover Day” delights all audiences. It also shows what causes are important to your brand. I also try to link them to one of my products or blogs.” – @bharatloanwala

3. Behind the scenes

“As the owner of an apparel brand, I have found several things key in gaining a social following but one that has been quite crucial has been showing behind the scenes. I think the beauty of social media is being able to really connect with customers and followers, and one of the most effective ways to do that is to make them a part of the process, sharing the stories behind the curtain.” –Dalia MacPhee, DALIA MACPHEE

4. Funny videos

“Video is hugely popular on social media, so if you want more followers, you need to be creating and sharing more video content. Remember though, your videos have to be short and they’ve got to grab the viewer right away since many users admit to only watching the first 30 seconds of a video or so. Plus, if your video is funny, users will be more likely to share it and tag their friends.” –Chris Christoff, MonsterInsights

5. Live video

“Live video is an awesome and easy way to get more followers on social media. Live video on Facebook or Instagram is way more interactive: Viewers can watch you in real time and talk to you in the live comment section. It’s great for forming a more personal connection with your audience and increasing your organic reach. You can introduce your team, take viewers on a tour and so much more.” – Blair Williams, MemberPress

6. How-to videos

“I find that providing your followers value can lead to a greater conversation around you and your brand. How-to videos are the best examples of this, or at the very least, a high-level discussion of the best practices in your industry. Really any piece of educational content that you can make engaging and simplify for your audience will lead others to you as a thought leader in your industry.” –Kristopher Brian Jones, LSEO.com

7. List articles

“Also known as “listicles,” these articles containing lists are great for sharing on social because they are very quick to digest, and are often informative and interesting. It’s a good way to get engagement and people will follow you if they like your content!” – Baruch Labunski, Rank Secure

8. Content that shows vulnerability

“Whether as brands or individuals, there’s obvious value in creating content that shares expertise and thought leadership. I’’m always surprised by how much more people respond to questions or stories that show genuine vulnerability (e.g., the struggle that led to X versus just X by itself).” – Sam Saxton, Paragon Stairs

9. Content that solves problems

“My goal is to solve one person’s problem a day; this helps me win trust and rapport for my brand. This also gets them to recommend me and help build my community when I have started from scratch. At the same time, I am doing what I have always intended to do which is deliver value. When you deliver value, you will win a new audience every time. Solve a problem a day.” –Sweta Patel, Startup Growth Mode

10. Links to case studies

“I find that case studies are especially good for attracting highly targeted followers. These may be people who are already customers or who are likely to sign up for our services. Case studies, either showcasing our products or something relevant to our industry, provide decision-makers with tangible proof that something works.” –Kalin Kassabov, ProTexting

“In our niche, our highest performing articles are how-to guides and funnily enough, collections of memes. Sometimes giving your consumer an opportunity to take a mental break instead of trying to cram ‘useful’ content down their throat will build positive brand associations, and they’ll be more likely to follow you. These days, everyone is trying to solve your problems to get you to notice them. 2019

Force Multipliers are tools that help you amplify your effort to produce more output. A hammer is a force multiplier. Investing in Force Multipliersmeans that you’ll get more done with the same amount of effort and time.

To be successful in business, you need to input energy and time.

Energy and time seem finite. We never seem to have enough…

How can we hack this equation?

Through the use of a “Force Multiplier”.

Here’s two equations to make it simple:

[Energy] x [Time] = [Results] — (this is without a force multiplier).

[Energy]^FM x [Time]^FM = [Results] — (this is with a force multiplier).

Most people try to get more results by working more hours and optimizing their body to get more energy. This works, and you should do it. But it reaches a limit based on the biological thresholds of our human system.

Once you get to that limit. it’s time to start playing with force multipliers.

One of the most powerful force multipliers I know is FOCUS.

And one of the most powerful methods to improve focus is to work in a team of people who have the same goals and dreams.

In our business training we combine people all over the world who work together to launch an online business that is based on selling digital products online. @bharatloanwala

A Bank Guarantee vs. a Letter of Credit: An Overview

A bank guarantee and a letter of credit are both promises from a financial institution that a borrower will be able to repay a debt to another party, no matter what the debtor’s financial circumstances. While different, both bank guarantees and letters of credit assure a third party that if the borrowing party can’t repay what it owes, the financial institution will step in on behalf of the borrower. By providing financial backing for the borrowing party (often at the request of the other one), these promises serve to reduce risk factors, encouraging the transaction to proceed. But they work in slightly different ways and in different situations.

Letters of credit are especially important in international trade due to the distance involved, the potentially differing laws in the countries of the businesses involved, and the difficulty of the parties meeting in person. While letters of credit are used mostly in global transactions, bank guarantees are often used in real estate contracts and infrastructure projects.

A Bank Guarantee

Bank guarantees represent a more significant contractual obligation for banks than letters of credit do. A bank guarantee, like a letter of credit, guarantees a sum of money to a beneficiary; however, unlike a letter of credit, the sum is only paid if the opposing party does not fulfill the stipulated obligations under the contract. This can be used to essentially ensure a buyer or seller from loss or damage due to nonperformance by the other party in a contract.

Bank guarantees protect both parties in a contractual agreement from credit risk.

For instance, a construction company and its cement supplier may enter into a new contract to build a mall. Both parties may have to issue bank guarantees to prove their financial bona fides and capability. In a case where the supplier fails to deliver cement within a specified time, the construction company would notify the bank, which then pays the company the amount specified in the bank guarantee.

A Letter of Credit

Sometimes referred to as a documentary credit, a letter of credit acts as a promissory note from a financial institution, usually a bank or credit union. It guarantees a buyer’s payment to a seller or a borrower’s payment to a lender will be received on time and for the full amount. It also states that if the buyer can’t make payment on the purchase, the bank will cover the full or remaining amount owed.

A letter of credit represents an obligation taken on by a bank to make a payment once certain criteria are met. After these terms are completed and confirmed, the bank will transfer the funds. The letter of credit ensures the payment will be made as long as the services are performed.

For example, say a U.S. wholesaler receives an order from a new client, a Canadian company. Because the wholesaler has no way of knowing whether this new client can fulfill its payment obligations, it requests a letter of credit is provided in the purchasing contract.

The purchasing company applies for a letter of credit at a bank where it already has funds or a line of credit (LOC). The bank issuing the letter of credit holds payment on behalf of the buyer until it receives confirmation that the goods in the transaction have been shipped. After the goods have been shipped, the bank would pay the wholesaler its due as long as the terms of the sales contract are met, such as delivery before a certain time or confirmation from the buyer that the goods were received undamaged.

Basically, the letter of credit substitutes the bank’s credit for that of its client, ensuring correct and timely payment.

Special Considerations

Both bank guarantees and letters of credit work to reduce the risk in a business agreement or deal. Parties are more likely to agree to the transaction because they have less liability when a letter of credit or bank guarantee is active. These agreements are particularly important and useful in what would otherwise be risky transactions, such as certain real estate and international trade contracts.

Banks thoroughly screen clients interested in one of these documents. After the bank has determined that the applicant is creditworthy and has a reasonable risk, a monetary limit is placed on the agreement. The bank agrees to be obligated up to, but not exceeding, the limit. This protects the bank by providing a specific threshold of risk.

One might say letters of credit ensure a transaction proceeds as planned, while bank guarantees reduce the loss if the transaction doesn’t go as planned.

Key Takeaways

A bank guarantee is a promise from a lending institution that ensures that if a debtor can’t cover a debt, the bank will step up.

Letters of credit are also financial promises on behalf of one party in a transaction and are especially significant in international trade.

Bank guarantees are often used in real estate contracts and infrastructure projects, while letters of credit are used mostly in global transactions.@bharatloanwala

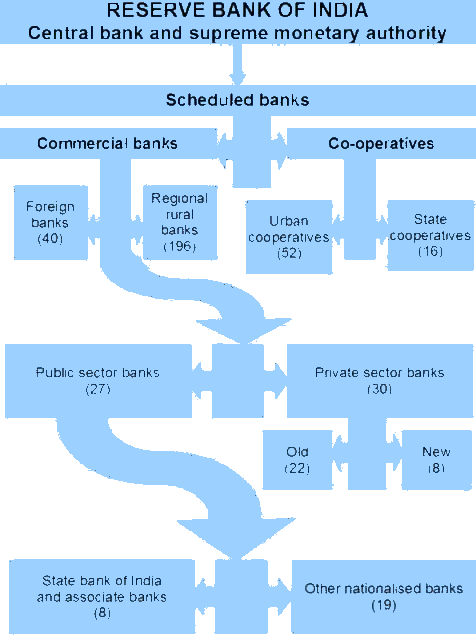

The country had no central bank prior to the establishment of the RBI. The RBI is the supreme monetary and banking authority in the country and controls the banking system in India. It is called the Reserve Bank’ as it keeps the reserves of all commercial banks.

Scheduled & Non –scheduled Banks

A scheduled bank is a bank that is listed under the second schedule of the RBI Act, 1934. In order to be included under this schedule of the RBI Act, banks have to fulfill certain conditions such as having a paid up capital and reserves of at least 0.5 million and satisfying the Reserve Bank that its affairs are not being conducted in a manner prejudicial to the interests of its depositors. Scheduled banks are further classified into commercial and cooperative banks. Non- scheduled banks are those which are not included in the second schedule of the RBI Act, 1934. At present these are only three such banks in the country.

Commercial Banks

Commercial banks may be defined as, any banking organization that deals with the deposits and loans of business organizations.Commercial banks issue bank checks and drafts, as well as accept money on term deposits. Commercial banks also act as moneylenders, by way of installment loans and overdrafts.Commercial banks also allow for a variety of deposit accounts, such as checking, savings, and time deposit. These institutions are run to make a profit and owned by a group of individuals.

Scheduled Commercial Banks (SCBs):

Scheduled commercial banks (SCBs) account for a major proportion of the business of the scheduled banks. SCBs in India are categorized into the five groups based on their ownership and/or their nature of operations. State Bank of India and its six associates (excluding State Bank of Saurashtra, which has been merged with the SBI with effect from August 13, 2008) are recognised as a separate category of SCBs, because of the distinct statutes (SBI Act, 1955 and SBI Subsidiary Banks Act, 1959) that govern them. Nationalised banks and SBI and associates together form the public sector banks group IDBI ltd. has been included in the nationalised banks group since December 2004. Private sector banks include the old private sector banks and the new generation private sector banks- which were incorporated according to the revised guidelines issued by the RBI regarding the entry of private sector banks in 1993.

Foreign banks are present in the country either through complete branch/subsidiary route presence or through their representative offices.

Types of Scheduled Commercial Banks

Public Sector Banks

These are banks where majority stake is held by the Government of India. Examples of public sector banks are: SBI, Bank of India, Canara Bank, etc.

Private Sector Banks

These are banks majority of share capital of the bank is held by private individuals. These banks are registered as companies with limited liability. Examples of private sector banks are: ICICI Bank, Axis bank, HDFC, etc.

Foreign Banks

These banks are registered and have their headquarters in a foreign country but operate their branches in our country. Examples of foreign banks in India are: HSBC, Citibank, Standard Chartered Bank, etc

Regional Rural Banks

Regional Rural Banks were established under the provisions of an Ordinance promulgated on the 26th September 1975 and the RRB Act, 1976 with an objective to ensure sufficient institutional credit for agriculture and other rural sectors. The area of operation of RRBs is limited to the area as notified by GoI covering one or more districts in the State.

RRBs are jointly owned by GoI, the concerned State Government and Sponsor Banks (27 scheduled commercial banks and one State Cooperative Bank); the issued capital of a RRB is shared by the owners in the proportion of 50%, 15% and 35% respectively.

Prathama bank is the first Regional Rural Bank in India located in the city Moradabad in Uttar Pradesh.

Type of Commercial Banks

Major Shareholders

Major Players

Public Sector Banks

Government of India

SBI, PNB, Canara Bank, Bank of Baroda, Bank of India, etc

Private Sector Banks

Private Individuals

ICICI Bank, HDFC Bank, Axis Bank, Kotak Mahindra Bank, Yes Bank etc.

Foreign Banks

Foreign Entity

Standard Chartered Bank, Citi Bank, HSBC, Deutsche Bank, BNP Paribas, etc.

Regional Rural Banks

Central Govt, Concerned State Govt and Sponsor Bank in the ratio of 50 : 15 : 35

Andhra Pradesh Grameena Vikas Bank, Uttranchal Gramin Bank, Prathama Bank, etc.

Cooperative Banks

A co-operative bank is a financial entity which belongs to its members, who are at the same time the owners and the customers of their bank. Co-operative banks are often created by persons belonging to the same local or professional community or sharing a common interest. Co-operative banks generally provide their members with a wide range of banking and financial services (loans, deposits, banking accounts, etc).

They provide limited banking products and are specialists in agriculture-related products.

Cooperative banks are the primary financiers of agricultural activities, some small-scale industries and self-employed workers.

Co-operative banks function on the basis of “no-profit no-loss”.

Anyonya Co-operative Bank Limited (ACBL) is the first co-operative bank in India located in the city of Vadodara in Gujarat.

The co-operative banking structure in India is divided into following main 5 categories:

•

Primary Urban Co-op Banks

•

Primary Agricultural Credit Societies

•

District Central Co-op Banks

•

State Co-operative Banks

•

Land Development Banks

Difference between Scheduled Commercial and Schedule Co-operative Banks

The basic difference between scheduled commercial banks and scheduled cooperative banks is in their holding pattern. Scheduled cooperative banks are cooperative credit institutions that are registered under the Cooperative Societies Act. These banks work according to the cooperative principles of mutual assistance.Also,unlike commercial banks ,these banks work on the basis of “no-profit no-loss”.

How Banks Function

Banks make money by lending your money out at interest and by charging you for services provided. Banks keep on lending money.

The other big revenue items generated by banks are the fees they charge. Bank charge for every service, whether it is for an electronic transaction, or permitting a transfer through the Internet banking system.

The banking industry in India is highly regulated. Few important regulations are mentioned below:

Regulatory Requirements

A bank has to set aside a certain percentage of total funds to meet regulatory requirements. The primary regulatory ratios are Cash Reserve Ratio (CRR) and Statutory Liquidity Ratio (SLR). RBI uses both these instruments to regulate money supply in the economy.CRR is the percentage of net total of deposits a bank is required to maintain in form of cash with RBI. Currently this ratio is at 5.5%. This is used to control the liquidity in the economy. Higher the CRR, the lower is the amount that banks will be able to use for lending activities and vice versa.SLR is the minimum percentage of deposits that the bank has to maintain in form of gold, cash and/or other approved securities. Currently, the SLR is 24%. This is used to regulate the credit growth

The core operating income of a bank is interest income (comprises 75-85% in the total income of almost all Indian Banks). Besides interest income, a bank also generates fee-based income in the form of commissions and exchange, income from treasury operations and other income from other banking activities. As banks were assigned a special role in the economic development of the country, RBI has stipulated that a portion of bank lending should be for the development of under-banked and under-privileged sections, which is called the priority sector. Current rules stipulate that domestic banks should lend 40% and the foreign banks should lend 32% of their net credit to the priority sector. On the cost sides, the major items for a bank are interest paid on different types of deposits, bonds issued and borrowings, and provisioning cost for Non-performing Assets (NPAs).

Types of Businesses of Banks

The banking business can be broadly categorized into Retail Banking, Wholesale or Corporate Banking, Treasury Operations and Other Banking Activities.

Business Segmentation

Retail Banking

Loans to individuals (Housing loan, Auto loan, Education loan and other personal loan) or small businesses.

Wholesale banking

Loans to mid and large corporate (Project Finance, Working Capital Loans, Terms Loans, Lease Finance, etc.)

Treasury Operations

Investment in bonds, equity, Mutual Funds, commodities, derivatives; trading and forex operations

Other Banking Activities

Hire purchase activities, leasing business, merchant banking, Syndication services, etc.

Retail banking also known as Consumer Banking is the provision of services by a bank to individual consumers, rather than to companies, corporations or other banks. Services offered include savings and transactional accounts, mortgages, personal loans, debit cards, and credit cards. Retail banking segment is the highest margin business as compared to other business segments in the banking industry. Currently, ICICI Bank is the largest players in this segment in India. Other major players in this segment are SBI, PNB, HDFC Bank, etc.

Typical products offered by a retail bank include:

•

Savings /Current accounts

•

Debit cards

•

ATM cards

•

Credit cards

•

Traveler’s cheques

•

Mortgages

•

Home equity loans

•

Personal loans

•

Certificates of deposit/Term deposits

Wholesale banking is the provision of services by banks to organizations such as Mortgage Brokers, large corporate clients, mid-sized companies, real estate developers and investors, international trade finance businesses, institutional customer(such as pension funds and government entities/agencies), and services offered to other banks or other financial institutions.

Wholesale finance refers to financial services conducted between financial services companies and institutions such as banks, insurers, fund managers, and stockbrokers.

Modern wholesale banks engage in:

•

Finance wholesaling

•

Underwriting

•

Market making

•

Consultancy

•

Mergers and acquisitions

•

Fund management

Wholesale banking segment in India is largely dominated by large Indian banks – SBI, ICICI Banks, PNB, BoB, etc.

Treasury management (or treasury operations) includes management of an enterprise’s holdings, with the ultimate goal of managing the firm’s liquidity and mitigating its operational, financial and reputational risk. Treasury Management includes a firm’s collections, disbursements, concentration, investment and funding activities. In larger firms, it may also include trading in bonds, currencies, financial derivatives and the associated financial risk management. Most banks have whole departments devoted to treasury management and supporting their clients’ needs in this area

Bank Treasuries may have the following departments:

•

A Fixed Income or Money Market desk that is devoted to buying and selling interest bearing securities

•

A Foreign exchange or “FX” desk that buys and sells currencies

•

A Capital Markets or Equities desk that deals in shares listed on the stock market.

The banking system of India consists of the centralbank (Reserve Bank of India – RBI), commercial banks, cooperative banks and development banks(development finance institutions). These institutions, which provide a meeting ground for the savers and the investors, form the core of India’s financial sector.

Banking in India, in the modern sense, originated in the last decade of the 18th century. Among the first banks were the Bank of Hindustan, which was established in 1770 and liquidated in 1829–32; and the General Bank of India, established in 1786 but failed in 1791

In 1960, the State Banks of India was given control of eight state-associated banks under the State Bank of India (Subsidiary Banks) Act, 1959. These are now called its associate banks.[6] In 1969 the Indian governmentnationalised 14 major private banks, one of the big bank was Bank of India. In 1980, 6 more private banks were nationalised.[8] These nationalised banks are the majority of lenders in the Indian economy. They dominate the banking sector because of their large size and widespread networks.[9]

The Indian banking sector is broadly classified into scheduled and non-scheduled banks. The scheduled banks are those included under the 2nd Schedule of the Reserve Bank of India Act, 1934. The scheduled banks are further classified into: nationalised banks; State Bank of India and its associates; Regional Rural Banks (RRBs); foreign banks; and other Indian private sector banks.[7] The term commercial banks refers to both scheduled and non-scheduled commercial banks regulated under the Banking Regulation Act, 1949.[10]

Generally the supply, product range and reach of banking in India is fairly mature-even though reach in rural India and to the poor still remains a challenge. The government has developed initiatives to address this through the State Bank of India expanding its branch network and through the National Bank for Agriculture and Rural Development (NABARD) with facilities like microfinance.